Online banks that have traditionally offered super-high interest rates on their savings accounts are losing their primary attraction to customers. Banks such as ‘Ally’ have always offered a 3% interest rate on all savings accounts. Over the past few months, they have cut their interest rate by a drastic 73%. Now, they can only offer customers a 0.5% interest rate. Every other bank has also drastically cut their interest rates over the past few months. Why did they do this? What impact will this have?

Why does the Fed devalue our money?

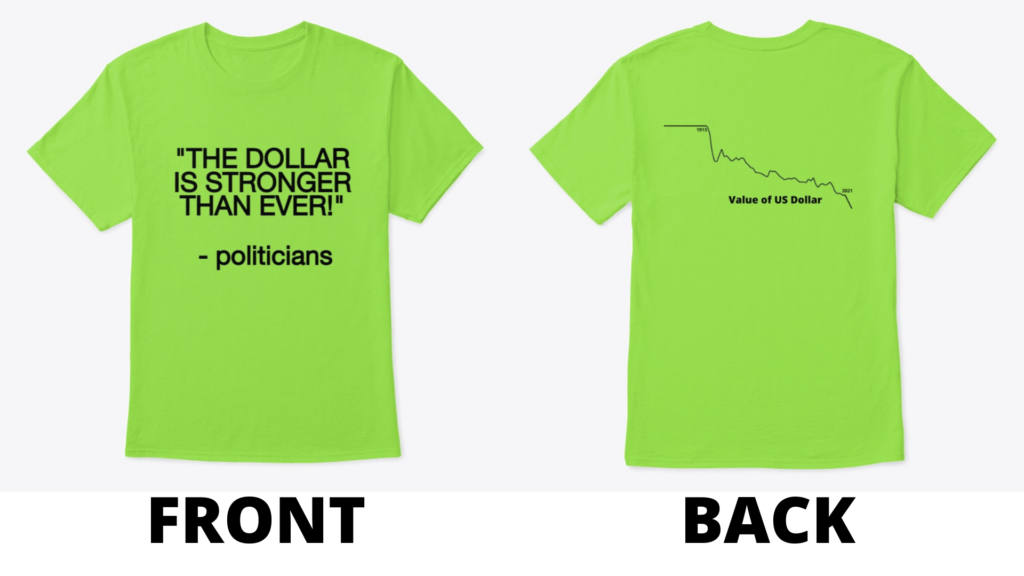

The federal reserve is the central bank of the US. It is not part of the US government, making it hardly accountable to voters. It is also not a private entity, meaning that it has no accountability to customers or other market forces. It stands alone in purgatory as an untouchable and omnipotent creator of money. According to the federal reserve, the US economy needs inflation. If people thought that their dollars would retain their value or maybe even increase in value, they would be more likely to save them and less likely to spend them. Without regular spending, the economy could suffer, according to the politicians and bankers who run the fed. Stated from another perspective, the Fed encourages spending and discourages saving.

The fed and their allies in DC have another massive incentive to devalue the US dollar. Because the US government debt is denominated in US dollars, they effectively decrease their debt by making dollars less valuable compared to other currencies and assets.

Personal savings

Many people are aware that the inflation created by the federal reserve and the US government at large is devastating for long-term savers. At around 2% inflation per year – which is generally the fed’s target rate – your $100,000 in savings will actually lose over 30% of its purchasing power over the next 20 years. Compounding the hardship for Americans hoping to retire one day, interest rates plummet along with the interest rate set by the federal reserve. So, your money is barely earning any interest by sitting in a bank. What should you do with your money if you want it to hold its value from now until you retire? You need to invest it.

The ‘overvalued’ stock market

As a result of banks becoming less attractive to savers due to the meager interest rates they could offer, savers have been forced to become investors. Over the past few months, many Americans have begun to shift their savings from their bank accounts into the stock market. Being that each ‘buy’ increases the price of the given security (stock or ETF), this has grossly inflated the price of many securities. The S&P 500 (an index comprised of the 500 largest public companies) just hit an all-time record high despite the US economy being crippled by the coronavirus. This is another indication that the US stock market is massively overvalued. People are investing much more money in the stock market than they would absent government intervention.

Hedging your bets

As I am not licensed by the government to give financial advice, consider the following to be ‘reading for entertainment’ and not ‘financial advice’:

What I would do to hedge against the inflation and other issues (and there are many issues I see occurring with the US dollar and the economy in the future) I would do the following with my savings: I would utilize a ‘super-diverse’ strategy involving investing in as many asset classes and concepts as possible. Store some of your value in gold, silver, copper (yes, the actual metals), guns, ammunition, property, vehicles, tools, stocks, ETFs, bonds, and invest in yourself. Of course, you can only fit so many guns and so much ammunition in your house. Once you maximize those investments, I would place a large chunk of my savings in index ETFs, other ETFs that I am optimistic about, and maybe into some companies that I am super confident will remain strong for a long time. If you do not want to risk your money, you are best off placing it into index ETFs such as the S&P 500 or the Nasdaq. They will almost certainly retain their value and will likely grow by a few percentage points each year.

I also must underscore the importance of investing in yourself. Invest in your health. Invest in your education. Whether the economy improves or worsens, the more educated you are, the more valuable you will be to employers and customers. Learn a language. Learn a new skill. Maybe even pick up a book and read it. The US government and their central bank can crush the economy and hinder savings accounts, but they can’t take away your valuable skills and knowledge.