In response to the horrendous monetary inflation by the federal government, the geniuses in DC have caused another major issue without significantly addressing inflation. As The Liberty Block has reported numerous times, the vast majority of all dollars ever printed in history were created over the past three years. Each dollar created by the Federal Reserve dilutes the purchasing power of the dollars in your wallet, bank account, and investment funds. On a simple level, doubling the amount of dollars in circulation cuts the value of each of your dollars in half.

The expansion of the amount of dollars in circulation (money supply) comes about in a few different ways. The federal government can borrow the money, print the money, or they can have their banks issue new loans. Because every bank is technically part of the Federal Reserve system, they are essentially a part of the government. One of the major ways the government controls the banks is by controlling interest rates. The DC politicians allow banks to expand the money supply (create new money) by giving people loans. Banks have always been required by law to maintain some cash reserves in their vaults, but that requirement was quietly repealed in 2020 behind the distractions of corona-fascism (something that few outlets other than The Liberty Block reported on). Thus, when a person takes a loan from a bank, the bank simply transfers the digital numbers to their account, effectively creating new money from thin air. This is a primary cause of monetary inflation. Borrowers are more likely to take out loans when the interest rates are low. If inflation is running at 10% per year and you could get a loan for 3% interest, it would be wise to borrow as much money as possible and convert it to any investment or asset that grows greater than 3% per year. Considering that the dollar is losing 10% of its value each year, any asset would do. To keep it simple, just buy gold or silver or park your money in an S&P fund or even a money-market account if you want zero risk.

The Federal Reserve, therefore, has the ability to control how quickly the money supply expands by adjusting interest rates. If you were going to borrow $300k for a house or a million dollars for a business venture, you would be much more likely to do so in a low-interest environment. As interest rates increase, you become less likely to apply for a loan from a bank. In this sense, higher interest rates are ‘good’ for the economy, because they technically help slow the rate of monetary inflation. On the other hand, higher interest rates deter new loans, making it harder for people to buy homes and cars and start or expand their businesses. A rapid increase in interest rates also causes severe harm to the banks.

To keep it as simple as possible:

- Banks hold money for customers (depositors)

- Banks offer depositors interest for their money

- Banks earn money on deposits by investing

- Those investments include new loans to borrowers and purchasing bonds

- A large portion of those bonds are long-term, like 30 years

- The older bonds are locked in at very low interest rates

- The bank holds 2% bonds and some other modest investments

- They can only give customers a 1.5% interest on their accounts

- But now the Fed increased interest rates to 8%.

- This means that the Fed offers bonds with much higher interest rates

- But the bank is locked in for decades longer at much lower interest rates

- So the banks cannot compete with the bonds

- Customers pull their money from the banks

- They’d now prefer to invest in bonds, stocks, or assets on their own

- The banks lost billions and have inadequate liquid cash reserves

- The liquidity crisis causes banks to collapse

- A run on the banks is likely imminent due to fear of bank collapses

- Pandemonium ensues

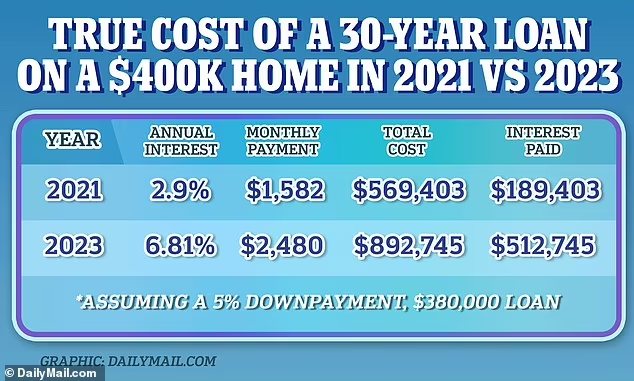

In their efforts to combat the terrible inflation, the Fed has been increasing rates consistently for the past two years. The rate is still far lower than inflation, so it probably isn’t doing much to help. But the higher interest rates make it much harder to buy new homes. For a 380k home, the massive increase in average interest rates from 3% to 7% over the past two years translates to the average home-buyer spending around $900 more per month to pay their mortgage. The increase in average monthly payments from $1,600 to $2,500 is going to crush the dreams of millions of Americans who hoped to buy a house.

The DC politicians and their cronies who run the banks caused the problem and their ‘solutions’ only cause more problems. There is no way to fix these tremendous issues with the American financial system. The only solution must involve a total separation from DC’s currency and banking scheme. Adopting and using alternative currencies such as silver, Goldbacks, and crypto are the simplest ways of achieving this. As the dollar crumbles, states will secede from the union or the DC Empire will collapse under the weight of its own tyranny, debt, and inflation.

This article does not necessarily reflect the opinions of The Liberty Block or any of its members. We welcome all forms of serious feedback and debate.